Picketty’s “Capital” reviewed

This dense 577-page analysis sold over 1.5 million copies because Piketty provides data warning today’s economy will return us to levels of inequality last seen in ruthless early-period capitalism. Commentary from the left and right was about detail and Picketty’s conclusions on trends in inequality proved robust (source 1 below) but some critics’ points were worth noting and are reproduced below.

Wealth inequality is very different to income inequality, becoming much more extreme over time, so Picketty proposes globally standard wealth taxes to restore balance which Galbraith claims are utopian in the US (source 3, part 3) and Solow supports (source 2);

There is no provable law of rising inequality (source 3, parts 1 & 2, seeking one is just as silly as claiming free markets are efficient.

(source 1) New Yorker magazine review by John Cassidy, March 26, 2014

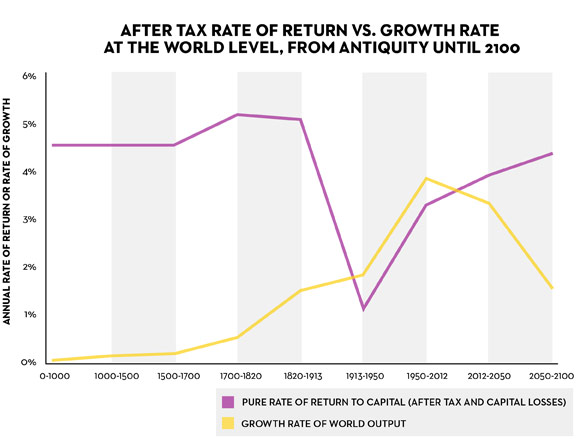

The important point to note is this: setting aside the period from the late nineteenth century to the early twenty-first century, which is roughly what we would call modernity, the growth rate has been below the rate of return, implying steadily rising inequality. The twentieth century, far from representing normality, was a historic exception that is unlikely to be repeated, Piketty argues. In the coming decades, he says, the growth rate will most likely fall back below the rate of return, and the “consequences for the long-term dynamics of the wealth distribution are potentially terrifying.”

The Financial Times was quick to criticise, alleging transcription errors and incorrect formulas in the spreadsheets provided by Prof Piketty to back up his book “Capital in the 21st Century”. It also said some of the data appeared to be cherry-picked or constructed without an original source, concluding there was “little evidence in Prof Piketty’s original sources to bear out the thesis that an increasing share of total wealth is held by the richest few”.

In response, Prof Picketty said the available data on wealth was “imperfect” but insisted there was widespread recognition that his central thesis was correct. “Where the Financial Times is being dishonest is to suggest that this changes things in the conclusions I make, when in fact it changes nothing. More recent studies only support my conclusions, by using different sources.”

The FT’s critique of his data sparked intense debate, as admirers and critics of the work scrambled to assess the impact of the data flaws on his thesis that wealth inequalities are heading back up to levels last seen before the first world war. Paul Krugman hailed Prof Piketty’s work as potentially the most important economics book of the decade, and dismissed the FT’s finding that there was “no obvious upward trend” in wealth concentration among the richest people over the last 50 years as evidence that the FT itself was “doing something wrong”.

(source 2) “Thomas Piketty Is Right: Everything you need to know about ‘Capital in the Twenty-First Century’” by Robert M Solow in New Republic, April 23, 2014

Piketty’s strong preference is for an annual progressive tax on wealth, worldwide if possible, to exclude flight to phony tax havens. He recognizes that a global tax is a hopeless goal, but he thinks that it is possible to enforce a regional wealth tax in an area the size of Europe or the United States. An example of the sort of rate schedule that he has in mind is 0 percent on fortunes below one million euros, 1 percent on fortunes between one and five million euros, and 2 percent above five million euros. (A euro is currently worth about $1.37.)

Remember that this is an annual tax, not a onetime levy. He estimates that such a tax applied in the European Union would generate revenue equal to about 2 percent of GDP, to be used or distributed according to some agreed formula. He seems to prefer, as would I, a slightly more progressive rate schedule. Of course the administration of such a tax would require a high degree of transparency and complete reporting on the part of financial institutions and other corporations. The book discusses in some detail how this might work in the European context. As with any tax, there would no doubt be a continuing struggle to close loopholes and prevent evasion, but that is par for the course.

Annual revenue of 2 percent of GDP is neither trivial nor enormous. But revenue is not the central purpose of Piketty’s proposal. Its point is that it is the difference between the growth rate and the after-tax return on capital that figures in the rich-get-richer dynamic of increasing inequality. A tax on capital with a rate structure like the one suggested would diminish the gap between the rate of return and the growth rate by perhaps 1.5 percent and would weaken that mechanism perceptibly.

This proposal makes technical sense because it is a natural antidote to the dynamics of inequality that he has uncovered. Keep in mind that the rich-get-richer process is a property of the system as it operates on already accumulated wealth. It does not work through individual incentives to innovate or even to save. Blunting it would not necessarily blunt them. Of course a lower after-tax return on capital might make the accumulation of large fortunes somewhat less attractive, though even that is not at all clear. In any case, it would be a tolerable consequence.

Piketty writes as if a tax on wealth might sometime soon have political viability in Europe, where there is already some experience with capital levies. I have no opinion about that. On this side of the Atlantic, there would seem to be no serious prospect of such an outcome. We are politically unable to preserve even an estate tax with real bite. If we could, that would be a reasonable place to start, not to mention a more steeply progressive income tax that did not favor income from capital as the current system does. But the built-in tendency for the top to outpace everyone else will not yield to minor patches. Wouldn’t it be interesting if the United States were to become the land of the free, the home of the brave, and the last refuge of increasing inequality at the top (and perhaps also at the bottom)? Would that work for you?

Robert M. Solow is Institute Professor of Economics emeritus at MIT. He won the Nobel Prize in Economics in 1987.

(source 3) Kapital for the Twenty-First Century? Review by James K. Galbraith, Dissent Magazine, Spring 2014:

His approach is in two parts. First, he conflates physical capital equipment with all forms of money-valued wealth, including land and housing, whether that wealth is in productive use or not. He excludes only what neoclassical economists call “human capital,” presumably because it can’t be bought and sold. Then he estimates the market value of that wealth. His measure of capital is not physical but financial.

This, I fear, is a source of terrible confusion. Much of Piketty’s analysis turns on the ratio of capital—as he defines it—to national income: the capital/income ratio. It should be obvious that this ratio depends heavily on the flux of market value. And Piketty says as much. For example, when he describes the capital/income ratio plummeting in France, Britain, and Germany after 1910, he is referring only in part to physical destruction of capital equipment. There was almost no physical destruction in Britain during the First World War, and that in France was vastly overstated at the time, as Keynes showed in 1919. There was also very little in Germany, which was intact until the war’s end.

So what happened? The movement of Piketty’s ratio was largely due to much higher incomes, produced by wartime mobilization, in relation to the existing market cap, whose gains were restricted or fell during and after the war. Later, when asset values collapsed during the Great Depression, it mainly wasn’t physical capital that disintegrated, only its market value. During the Second World War, destruction played a larger role. The problem is that while physical and price changes are obviously different, Piketty treats them as if there were aspects of the same thing.

The evolution of inequality is not a natural process.

Piketty goes on to show that in relation to current income, the market value of capital assets has risen sharply since the 1970s. In the Anglo-American world, he calculates, this ratio rose from 250–300 percent of income at that time to 500–600 percent today. In some sense, “capital” has become more important, more dominant, a bigger factor in economic life.

Piketty attributes this rise to slower economic growth in relation to the return on capital, according to a formula he dubs a “fundamental law.” Algebraically, it is expressed as r>g, where r is the return on capital and g is the growth of income. Here again, he seems to be talking about physical volumes of capital, augmented year after year by profit and saving.

But he isn’t measuring physical volumes, and his formula does not explain the patterns in different countries very well. For instance, his capital-income ratio peaks for Japan in 1990—almost a quarter century ago, at the start of the long Japanese growth slump—and for the United States in 2008. Whereas in Canada, which did not have a financial crash, it’s apparently still rising. A simple mind might say that it’s market value rather than physical quantity that is changing, and that market value is driven by financialization and exaggerated by bubbles, rising where they are permitted and falling when they pop.

Piketty wants to provide a theory relevant to growth, which requires physical capital as its input. And yet he deploys an empirical measure that is unrelated to productive physical capital and whose dollar value depends, in part, on the return on capital. Where does the rate of return come from? Piketty never says. He merely asserts that the return on capital has usually averaged a certain value, say 5 percent on land in the nineteenth century, and higher in the twentieth.

The basic neoclassical theory holds that the rate of return on capital depends on its (marginal) productivity. In that case, we must be thinking of physical capital—and this (again) appears to be Piketty’s view. But the effort to build a theory of physical capital with a technological rate-of-return collapsed long ago, under a withering challenge from critics based in Cambridge, England in the 1950s and 1960s, notably Joan Robinson, Piero Sraffa, and Luigi Pasinetti.

Piketty devotes just three pages to the “Cambridge-Cambridge” controversies, but they are important because they are wildly misleading. He writes: “Controversy continued . . . between economists based primarily in Cambridge, Massachusetts (including [Robert] Solow and [Paul] Samuelson) . . . and economists working in Cambridge, England . . . who (not without a certain confusion at times) saw in Solow’s model a claim that growth is always perfectly balanced, thus negating the importance Keynes had attributed to short-term fluctuations. It was not until the 1970s that Solow’s so-called neoclassical growth model definitively carried the day”.

But the argument of the critics was not about Keynes, or fluctuations. It was about the concept of physical capital and whether profit can be derived from a production function. In desperate summary, the case was three-fold. First: one cannot add up the values of capital objects to get a common quantity without a prior rate of interest, which (since it is prior) must come from the financial and not the physical world. Second, if the actual interest rate is a financial variable, varying for financial reasons, the physical interpretation of a dollar-valued capital stock is meaningless. Third, a more subtle point: as the rate of interest falls, there is no systematic tendency to adopt a more “capital-intensive” technology, as the neoclassical model supposed.

In short, the Cambridge critique made meaningless the claim that richer countries got that way by using “more” capital. In fact, richer countries often use less apparent capital; they have a larger share of services in their output and of labor in their exports—the “Leontief paradox.” Instead, these countries became rich—as Pasinetti later argued—by learning, by improving technique, by installing infrastructure, with education, and—as I have argued—by implementing thoroughgoing regulation and social insurance. None of this has any necessary relation to Solow’s physical concept of capital, and still less to a measure of the capitalization of wealth in financial markets.

There is no reason to think that financial capitalization bears any close relationship to economic development. Most of the Asian countries, including Korea, Japan, and China, did very well for decades without financialization; so did continental Europe in the postwar years, and for that matter so did the United States before 1970. And Solow’s model did not carry the day. In 1966 Samuelson conceded the Cambridge argument!

(3, excerpt 2)

The empirical core of Piketty’s book is about the distribution of income as revealed by tax records in a handful of rich countries—mainly France and Britain but also the United States, Canada, Germany, Japan, Sweden, and some others. Its virtues lie in permitting a long view and in giving detailed attention to the income of elite groups, which other approaches to distribution often miss.

Piketty shows that in the mid-twentieth century the income share accruing to the top-most groups in his countries fell, thanks mainly to the effects and after-effects of the Second World War. These included unionization and rising wages, progressive income tax rates, and postwar nationalizations and expropriations in Britain and France. The top shares remained low for three decades. They then rose from the 1980s onward, sharply in the United States and Britain and less so in Europe and Japan.

Wealth concentrations seem to have peaked around 1910, fallen until 1970, and then increased once again. If Piketty’s estimates are correct, top wealth shares in France and the United States remain today below their Belle Époque values, while U.S. top income shares have returned to their values in the Gilded Age. Piketty also believes the United States is an extreme case—that income inequality here today exceeds that in some major developing countries, including India, China, and Indonesia.

How original and how reliable are these measures? Early on, Piketty makes a claim to be the sole living heir of Simon Kuznets, the great midcentury scholar of inequalities. He writes:

Oddly, no one has ever systematically pursued Kuznets’s work, no doubt in part because the historical and statistical study of tax records falls into a sort of academic no-man’s land, too historical for economists and too economistic for historians. That is a pity, because the dynamics of income inequality can only be studied in a long-run perspective, which is possible only if one makes use of tax records.

The statement is incorrect. Tax records are not the only available source of good inequality data. In research over twenty years, this reviewer has used payroll records to measure the long-run evolution of inequalities; in a paper published back in 1999, Thomas Ferguson and I tracked such measures for the United States to 1920—and we found roughly the same pattern as Piketty finds now.*

It is good to see our results confirmed, for this underscores a point of great importance. The evolution of inequality is not a natural process. The massive equalization in the United States between 1941 and 1945 was due to mobilization conducted under strict price controls alongside confiscatory top tax rates. The purpose was to double output without creating wartime millionaires. Conversely, the purpose of supply-side economics after 1980 was (mainly) to enrich the rich. In both cases, policy largely achieved the effect intended.

Under President Reagan, changes to U.S. tax law encouraged higher pay to corporate executives, the use of stock options, and (indirectly) the splitting of new technology firms into separately capitalized enterprises, which would eventually include Intel, Apple, Oracle, Microsoft, and the rest. Now, top incomes are no longer fixed salaries but instead closely track the stock market. This is the simple result of concentrated ownership, the flux in asset prices, and the use of capital funds for executive pay. During the tech boom, the correspondence between changing income inequality and the NASDAQ was exact, as Travis Hale and I show in a paper just published in the World Economic Review.

The lay reader will not be surprised. Academics, though, have to contend with the conventionally dominant work of (among others) Claudia Goldin and Lawrence Katz, who argue that the pattern of changing income inequalities in America is the result of a “race between education and technology” when it comes to wages, with first one in the lead and then the other. (When education leads, inequality supposedly falls, and vice versa.) Piketty pays deference to this claim but he adds no evidence in favor, and his facts contradict it. The reality is that wage structures change far less than profit-based incomes, and most of increasing inequality comes from an increasing flow of profit income to the very rich.

(3, exerprt 3)

To summarize so far, Thomas Piketty’s book about capital is neither about capital in the sense used by Marx nor about the physical capital that serves as a factor of production in the neoclassical model of economic growth. It is a book mainly about the valuation placed on tangible and financial assets, the distribution of those assets through time, and the inheritance of wealth from one generation to the next.

Why is this interesting? Adam Smith wrote the definitive one-sentence treatment: “Wealth, as Mr. Hobbes says, is power.” Private financial valuation measures power, including political power, even if the holder plays no active economic role. Absentee landlords and the Koch brothers have power of this type. Piketty calls it “patrimonial capitalism”—in other words, not the real thing.

The old system of high marginal tax rates was effective in its time. But would it work to go back to that system now? Alas, it would not.

Thanks to the French Revolution, registry of wealth and inheritance has been good in Piketty’s homeland for a long time. This allows Piketty to show how the simple determinants of the concentration of wealth are the rate of return on assets and the rates of economic and population growth. If the rate of return exceeds the growth rate, then the rich and the elderly gain in relation to everyone else. Meanwhile, inheritances depend on the extent to which the elderly accumulate—which is greater the longer they live—and on the rate at which they die. These two forces yield a flow of inheritances that Piketty estimates to be about 15 percent of annual income presently in France—astonishingly high for a factor that gets no attention at all in newspapers or textbooks.

Moreover, for France, Germany, and Britain, the “inheritance flow” has been rising since 1980, from negligible levels to substantial ones, due to a higher rate of return on financial assets along with a slightly rising mortality rate in an older population. The trend seems likely to continue—though one wonders about the effect of the financial crisis on valuations. Piketty also shows (to the small extent that data allow) that the share of global wealth held by a tiny group of billionaires has been rising much more rapidly than average global income.

What is the policy concern? Piketty writes:

[N]o matter how justified inequalities of wealth may be initially, fortunes can grow and perpetuate themselves beyond all reasonable limits and beyond any possible rational justification in terms of social utility. Entrepreneurs thus tend to turn into rentiers, not only with the passing of generations but even within a single lifetime. . . . [A] person who has good ideas at the age of forty will not necessarily still be having them at ninety, nor are his children sure to have any. Yet the wealth remains.

With this passage he makes a distinction that he previously blurred: between wealth justified by “social utility” and the other kind. It is the old distinction between “profit” and “rent.” But Piketty has removed our ability to use the word “capital” in this normal sense, to refer to the factor input that yields a profit in the “productive” sector, and to distinguish it from the source of income of the “rentier.”

As for remedy, Piketty’s dramatic call is for a “progressive global tax on capital”—by which he means a wealth tax. Indeed, what could be better suited to an age of inequality (and budget deficits) than a levy on the holdings of the rich, wherever and in whatever form they may be found? But if such a tax fails to discriminate between fortunes that have ongoing “social utility” and those that don’t—a distinction Piketty himself has just drawn—then it may not be the most carefully thought-out idea.

In any case, as Piketty admits, this proposal is “utopian.” To begin with, in a world where only a few countries accurately measure high incomes, it would require an entirely new tax base, a worldwide Domesday Book recording an annual measure of everyone’s personal net worth. That is beyond the abilities of even the NSA. And if the proposal is utopian, which is a synonym for futile, then why make it? Why spend an entire chapter on it—unless perhaps to incite the naive?

Piketty’s further policy views come in two chapters to which the reader is bound to arrive, after almost five hundred pages, a bit worn out. These reveal him to be neither radical nor neoliberal, nor even distinctively European. Despite having made some disparaging remarks early on about the savagery of the United States, it turns out that Thomas Piketty is a garden-variety social welfare democrat in the mold, largely, of the American New Deal.

How did the New Deal tackle the fortress of privilege that was the early twentieth-century United States? First, it built a system of social protections, including Social Security, the minimum wage, fair labor standards, conservation, public jobs, and public works, none of which had existed before. And the New Dealers regulated the banks, refinanced mortgages, and subdued corporate power. They built wealth shared in common by the community as a counterweight to private assets.

Another part of the New Deal (mainly in its later phase) was taxation. With war coming, Roosevelt imposed high progressive marginal tax rates, especially on unearned income from capital ownership. The effect was to discourage high corporate pay. Big business retained earnings, built factories and (after the war) skyscrapers, and did not dilute its shares by handing them out to insiders.

Piketty devotes only a few pages to the welfare state. He says very little about public goods. His focus remains taxes. For the United States, he urges a return to top national rates of 80 percent on annual incomes over $500,000 or $1,000,000. This may be his most popular idea in U.S. liberal circles nostalgic for the glory years. And to be sure, the old system of high marginal tax rates was effective in its time.

But would it work to go back to that system now? Alas, it would not. By the 1960s and ’70s, those top marginal tax rates were loophole-ridden. Corporate chiefs could compensate for low salaries with big perks. The rates were hated most by the small numbers who earned large sums with (mostly) honest work and had to pay them: sports stars, movie actors, performers, marquee authors, and so forth. The sensible point of the Tax Reform Act of 1986 was to simplify matters by imposing lower rates on a much broader base of taxable income. Raising rates again would not produce (as Piketty correctly states) a new generation of tax exiles. The reason is that it would be too easy to evade the rates, with tricks unavailable to the unglobalized plutocrats of two generations back. Anyone familiar with international tax avoidance schemes like the “Double Irish Dutch Sandwich” will know the drill.

If the heart of the problem is a rate of return on private assets that is too high, the better solution is to lower that rate of return. How? Raise minimum wages! That lowers the return on capital that relies on low-wage labor. Support unions! Tax corporate profits and personal capital gains, including dividends! Lower the interest rate actually required of businesses! Do this by creating new public and cooperative lenders to replace today’s zombie mega-banks. And if one is concerned about the monopoly rights granted by law and trade agreements to Big Pharma, Big Media, lawyers, doctors, and so forth, there is always the possibility (as Dean Baker reminds us) of introducing more competition.

Finally, there is the estate and gift tax—a jewel of the Progressive era. This Piketty rightly favors, but for the wrong reason. The main point of the estate tax is not to raise revenue, nor even to slow the creation of outsized fortunes per se; the tax does not interfere with creativity or creative destruction. The key point is to block the formation of dynasties. And the great virtue of this tax, as applied in the United States, is the culture of conspicuous philanthropy that it fosters, recycling big wealth to universities, hospitals, churches, theaters, libraries, museums, and small magazines.

These are the nonprofits that create about 8 percent of U.S. jobs, and whose services enhance the living standards of the whole population. Obviously the tax that fuels this philanthropy is today much eroded; dynasty is a huge political problem. But unlike the capital levy, the estate tax remains viable, in principle, because it requires that wealth be appraised only once, on the demise of the holder. Much more could be done if the law were tightened up, with a high threshold, a high rate, no loopholes, and less use of funds for nefarious politics, including efforts to destroy the estate tax.

In sum, Capital in the Twenty-First Century is a weighty book, replete with good information on the flows of income, transfers of wealth, and the distribution of financial resources in some of the world’s wealthiest countries. Piketty rightly argues, from the beginning, that good economics must begin—or at least include—a meticulous examination of the facts. Yet he does not provide a very sound guide to policy. And despite its great ambitions, his book is not the accomplished work of high theory that its title, length, and reception (so far) suggest.

James K. Galbraith is professor at the Lyndon B. Johnson School of Public Affairs, the University of Texas at Austin, and author of the forthcoming book, The End of Normal.

Source: http://www.dissentmagazine.org/article/kapital-for-the-twenty-first-century