Trump sparks junk debt boom

Investors are piling into some of the riskiest bonds sold by US companies as they bet on President Donald Trump delivering on his promises of a stronger economy, lower taxes and less regulation.

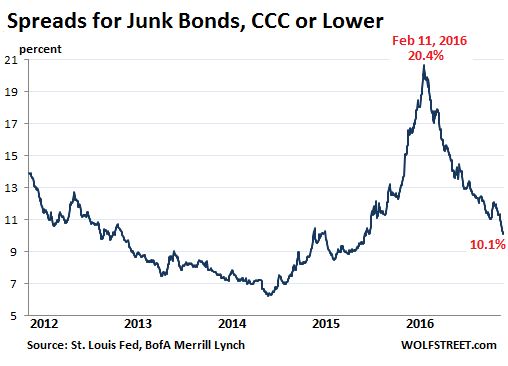

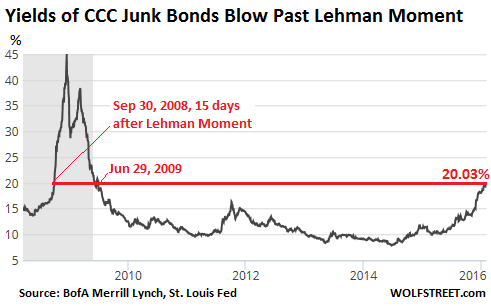

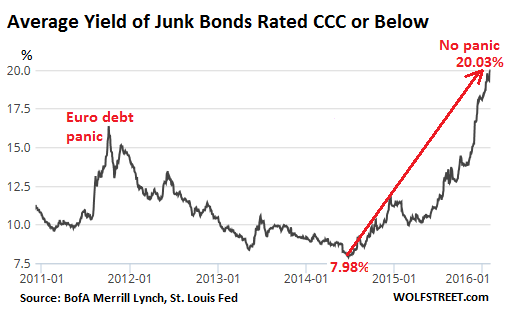

Demand for junk-rated bonds has driven yields on debt with the lowest quality credit rating down towards 10 per cent as more than $10bn has flowed into funds that invest in the asset class since the start of December. Borrowings by triple-C rated groups, among the lowest tier of the high-yield universe, have risen nearly two-thirds from a year earlier when the average yield for this part of the junk market peaked at 21.7 per cent. Yields fall as bond prices rise.

The current market rally has allowed the extension of credit to riskier borrowers at appealing terms, with high-yield groups raising a total of $41bn in the US so far this year, including money to refinance older debt — the greatest amount for a comparable period since 2013, according to Dealogic.

The “Trumpflation Trade” has driven investors into the asset class and pushed the risk premium they demand to own the bonds back down to levels last seen in 2014. Lower corporate taxes would free cash up for interest payments by these companies, while a reduced regulatory burden could bolster margins, investors and strategists say.

Bullish investor sentiment, however, comes as warnings mount over the outlook for the $2.2tn US junk bond market, led by a looming $1tn “maturity wall” facing lower rated companies over the next five years, a record level according to rating agency Moody’s.

The maturities peak in 2021, when more than $400bn of bonds and bank loans come due. At the same time, analysts with the credit agency warn that ratings on the loans have “deteriorated significantly. It is becoming impossible to ignore downside fundamental and political risks,” said Stephen Caprio, a strategist with UBS.

“Bank and nonbank lending standards are not easing, credit card and auto loan delinquencies are rising, bank commercial and industrial loan growth has stalled, and more protectionist sentiment is being underpriced in our view as a macro risk.”

The recent tempering of inflation expectations — in part due to weaker than expected US wage gains in January — has added to credit’s allure, as yields on the securities look more attractive than haven assets. This is Trump’s new world – buy risky debt for short-term profit, don’t invest in production. And this is what to junk bonds in the GFC…

Sources: Eric Platt New York Financial Times Feb 9 2017 in AFR https://www.ft.com

http://www.theaustralian.com.au